————————————————————————————————

Monthly Discussion

Six Years of Trend Detection

This Newsletter

has been in operation for six years but has now come to an end. In this last

issue I present an overview of the most important topics discussed during the

last six years. Because the trends investigated have generally been long-term

trends they are expected to be valid for some time into the future.

General Trends

Natural gas replaces

oil[1]

In the large

energy picture natural gas has been and will continue to replace oil as a

primary energy source. The rate of this replacement has fallen short from what

had been forecasted 15 years ago but nevertheless this substitution will continue

into the future because natural gas has higher energy content (i.e. more

hydrogen atoms per pound) than oil does.

When will

hydrogen come?[2]

Hydrogen is the

fuel with the highest energy content and consequently will eventually become

the ultimate fuel for humans. However, it does not constitute a primary

energy source because energy is required to produce it. Today most hydrogen is

produced by burning oil (and/or gas). But for the enormous quantities of

hydrogen that will be required in the future nuclear energy is the most likely

primary energy source to be used. It is no surprise that nuclear energy is

slowly but steadily coming back. It will eventually replace natural gas.

Hydrogen is overdue according to the

trend of a “natural” evolution toward fuels with higher energy content. The

amount of hydrogen used today as fuel is well below what it should be, so there

is some catching-up to be done. Watch this space, particularly in view of

recent efforts to produce hydrogen efficiently and cheaply from sunlight.

Supersonic

travel[3]

Supersonic air

travel has also fallen behind its 15-year-old forecasts and perhaps not

independently of the slowdowns mentioned above for natural gas and hydrogen.

After all, supersonic airplanes need a high-hydrogen-content fuel (i.e. liquid

gas or liquid hydrogen) and therefore their deployment has to await the

development of the corresponding engine technologies.

Magnetic

levitation trains (Maglevs)[4]

With the Shanghai

express put into operation on January 1, 2004 Maglevs were on schedule

according to the 15-year-old forecast made in Predictions. Maglevs are

expected to grow in order to substitute air travel in large-volume short air

routes. It took 50 years for railroads to go from 1% to 50% of their

development; it will take Maglevs a comparable amount of time and furthermore

Maglevs are not at the 1% level yet!

Western

economies[5]

The rate of growth

of American GDP has been slowing down since the mid 1990s and that of the

European Union is not doing better. That is because many large-scale

industrialization processes in the West (the construction of highways, the

construction of natural-gas pipelines, the growth of car populations, the

replacement of steamships with motors, the spreading of computers, etc.) have

reached completion all of them more or less at the same time. As a consequence

growth in the West cannot be at the levels it used to. But in the East (for

example in China) many of these processes have a long way to go before they

saturate, which puts China’s economy in a very competitive position.

The Kontradief cycle says that another

high-growth phase is due around the mid 2020s. But in view of the remarks of

the previous paragraph, the upcoming boom will be much more important in China

than in the West.

US involvement

in Iraq[6]

There are many

similarities between the US involvement in Viet Nam and in Iraq both in the

size of the timeframes and in the rates of development. The only difference is

in the absolute numbers. American casualties in Viet Nam reached 45,000 whereas

in Iraq they are expected to be ten times less.

The end of the

Internet rush[7]

The number of

Internet users has stopped growing worldwide. In developed countries this

number stopped growing because all people prone to become Internet users have

already done so (68% of the American population 45% of the European

population). In the rest of the world the number of Internet users is only 8%

of the population and yet it is not growing! That is because infrastructures

(electricity, telephones, education, etc.) are missing. It will be a long time

before people there become Internet users.

Rate of change

in our Lives[8]

The accelerating

rate of change in technology, medicine, information exchange, and other social

aspects of our life have misled many people who became alarmists and are now

drawing conclusions about runaway trends, imminent singularities, catastrophes

and the like. In a study of the appearance of turning points in the evolution

of the Universe (the 28 most significant cosmic milestones) I have concluded

that the Universe's complexity has been growing along a large-scale

natural-growth pattern that has just reached its mid point. The rate of change

in the future will therefore be slowing down from now onward, albeit very

gently. Complexity's life cycle peaks during the lifetime of people born in the

mid 1940s. It so happens that we are traversing a time in the world's history

that witnesses the largest amount of change ever.

We happen to be positioned at the world's

prime!

Stock-Market Trends

This newsletter

has carried discussions on many stock-market issues. Below I summarize the

conclusions that will be valid only in the long-term future.

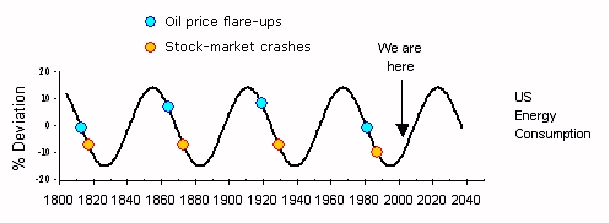

The Price of Oil[9]

It was pointed out

during the early days of the Newsletter that energy is the ultimate food for

life, which makes the price of oil something next to being sacred. Doubling the

price of bread in a large poor country could result in a popular uprising, or

trigger a revolution. Society on the other hand has ways of safeguarding its

survival. It has been argued that society possesses wisdom that surpasses the

wisdom of its individual members. It then makes sense to expect that society

manage to maintain the price of primary energy rather stable over time.

The price of primary energy has been seen

to flare-up in synch with Kondratief’s cycle, see Exhibit 3 below. In between

flare-ups the price of energy is confined to a reasonably stable window, say

$20 - $40 1996 dollars per barrel. The price of oil may seem excessive

recently, but when accounted for inflation and the weakness of the dollar, it

conforms to the above thinking.

Similarly for stock-market crashes. They

have their time in the Kondratief cycle and whether they are catastrophic like

in 1929 or more ephemeral like in 1987, the next one should be around 1940.

The Kondratief Cycle

Exhibit 3. Taken from the discussion of Newsletter issue of November 19, 2001, this graph needs no updating. It leaves no room for a near-future real flare-up of the price of oil, like that of 1981.

The Halloween

indicator[10]

It was

in Beating the Dow by O’Higgins that I first heard of the stock market’s

seasonal behavior, namely that 85% of gains with the DJIA (just capital gains,

not dividends) occur between October 31 and April 30. Since then I have

confirmed and monitored the evolution of this seasonality. It still works

today. I exploit it myself to halve my exposure to the whims of the stock

market. But beware of the EMH (see below), by the time that many investors try

to exploit this asymmetry of the stock market, the effect will evaporate.

The

Efficient Market Hypothesis[11]

The

Efficient Market Hypothesis (EMH) argues that all information available is

already reflected in the price of the stock. It essentially says that there can

be no secret successful schemes in the stock market. EMH comes in several

versions. In its strongest wording it says that no matter where you get your

information, it will sooner or later prove useless in obtaining

better-than-market-average investment results.

In its ultimate application the EMH could be behind

the grandfatherly advice “if you hold out long enough, the market will reward

you.” Have investors exploited this pattern sufficiently to render it useless?

Yes, there is some evidence in that direction. Record numbers of investors have

rushed to the stock market during the last 10-15 years and most of them are

stubbornly holding onto their stocks waiting for the market upturn. This could

be part of the reason the market has been and will remain horizontal for an

extended period of time, see long-term forecast (red line) in Exhibit 1.